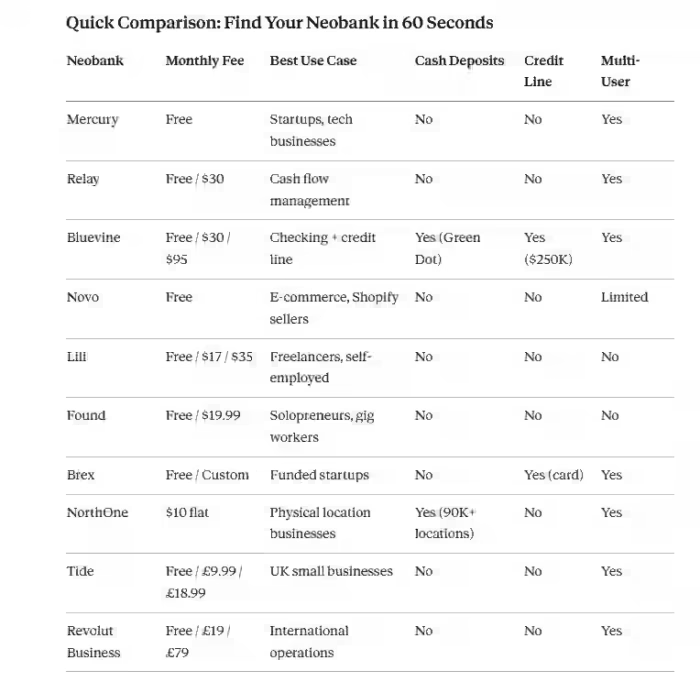

The best neobanks for small businesses in 2026 are Mercury, Relay, Bluevine, Novo, Lili, Found, Brex, NorthOne, Tide, and Revolut Business. Each one targets a different kind of small business owner, from solo freelancers who need clean expense tracking to fast-growing startups that need multi-user banking with built-in credit lines.

Neobanks are not all built the same way, and picking the wrong one costs you more than just monthly fees. It costs you time, flexibility, and sometimes access to your own money when you need it most.

Small business banking has been quietly broken for years. Traditional banks charge $20 to $40 a month for basic business checking, make you visit a branch to open an account, hold deposits for days without explanation, and offer customer support that routes you through four phone trees before you reach someone who can actually help. A 2024 survey by Bain & Company found that small business satisfaction with traditional banks sits at an all-time low, with nearly 60% of SMB owners saying their bank doesn’t understand the specific needs of small businesses.

Neobanks stepped into that gap. Most offer free or low-cost accounts, instant account opening, mobile-first design, and integrations with the tools small businesses already use, like QuickBooks, Stripe, and Shopify. According to Statista (2025), the global neobanking market is projected to grow past $722 billion by 2028, with small business accounts representing the fastest-growing segment.

So which one is actually right for your business? Let’s break it down honestly.

What Makes a Neobank Worth Using?

Before jumping into the list, it helps to know what we actually evaluated. Because “best” means completely different things to a solo freelancer versus a 12-person e-commerce business.

We assessed each neobank across five dimensions: fee structure, account features, integration with business tools, customer support quality, and suitability by business type. We also looked at real user reviews from the App Store, Google Play, and Trustpilot as of early 2026, alongside analysis from financial comparison platforms.

One observation worth flagging early: some neobanks marketed to small businesses are actually built for freelancers and side hustlers, not for businesses with employees, payroll, and multiple revenue streams. That distinction matters enormously when you’re choosing a primary business account.

For a broader look at how modern financial tools are reshaping small business operations, our guide to fintech tools for businesses covers the full ecosystem beyond banking alone.

Top 10 Best Neobanks for Small Business in 2026

1. Mercury

Best for: Tech startups, e-commerce, venture-backed businesses. Monthly fee: Free (Treasury and Raise products are paid). FDIC insured: Yes (via partner banks)

Mercury has quietly become the go-to neobank for startups, and it’s easy to see why when you actually use it. The account opens in minutes, supports multiple team members with customisable permissions, and comes with a clean dashboard that actually shows you useful financial data rather than just a transaction list.

The free checking account includes unlimited transactions, no minimum balance requirements, physical and virtual debit cards, and API access for developers who want to automate financial workflows. That last feature sounds niche, but for tech-forward businesses, it’s genuinely useful.

Mercury’s Treasury product lets you earn yield on idle cash by sweeping it into money market funds, which is something most traditional small business accounts don’t offer at all. For businesses holding significant cash reserves, that’s meaningful passive income with essentially zero effort.

The honest limitation: Mercury doesn’t offer cash deposits. If your business takes any cash payments, you’ll need a workaround. Mercury also doesn’t have a lending product in 2026, so if you need a credit line alongside your checking, you’re looking at a separate application elsewhere.

Best for: Startups and growing businesses that operate digitally, move money frequently, and want a bank account that integrates with their existing tech stack.

2. Relay

Best for: Service businesses, agencies, businesses using the profit-first methodology. Monthly fee: Free; Pro at $30/month. FDIC insured: Yes (via Thread Bank)

Relay is probably the most underrated neobank on this list. It lets you create up to 20 individual checking accounts and 50 virtual debit cards under one login, all at no cost on the free plan. That structure was built specifically for business owners who use systems like the Profit First method, where you divide revenue into separate, purpose-built accounts (profit, taxes, operating expenses, owner pay).

For service-based businesses and agencies that deal with irregular cash flow and multiple revenue streams, having named accounts for different purposes without paying for separate bank accounts is genuinely game-changing. You can see at a glance how much sits in your tax account, your payroll reserve, and your operating budget, all in one dashboard.

The Pro plan ($30/month) adds auto-transfer rules, which let you automatically move percentages of incoming revenue into your designated accounts the moment money hits. Set it once, forget it, and your cash flow organisation runs on autopilot.

Relay integrates directly with QuickBooks Online and Xero, which matters for businesses that want their banking and accounting synced without manual CSV exports. For small businesses still using spreadsheets, pairing Relay with one of the best QuickBooks alternatives is worth exploring before committing to an accounting workflow.

Best for: Service businesses, consultancies, and agencies that want structured cash management without paying for multiple bank accounts.

3. Bluevine

Best for: Businesses needing both checking and business credit. Monthly fee: Free; Plus at $30/month; Premier at $95/month. FDIC insured: Yes (via Coastal Community Bank)

Bluevine does something no other neobank on this list does as cleanly: it combines a genuinely solid business checking account with access to a revolving line of credit up to $250,000. For small businesses that deal with inventory gaps, project float, or seasonal revenue dips, that combination in one place is significant.

The free checking account earns 2.0% APY on balances up to $250,000 (as of Q1 2026, rate subject to change), which is well above what traditional banks pay on business accounts. There are no monthly fees on the base plan, no minimum balance requirements, and unlimited transactions.

The credit line application happens within the same platform. Approval decisions are typically within minutes for businesses that qualify. Terms are 6 or 12 months with weekly repayments. It’s not a replacement for an SBA loan, but for short-term working capital needs, it’s one of the fastest and most accessible options available to small businesses in 2026.

According to Forbes Advisor’s 2025 small business banking review, Bluevine ranked as one of the top three neobanks for businesses with credit needs, specifically because the integrated model reduces friction compared to applying for credit at a separate institution.

Best for: Small businesses that want interest-bearing checking plus access to flexible credit in one place, especially those with seasonal or project-based revenue patterns.

4. Novo

Best for: E-commerce sellers, freelancers, small retail businesses. Monthly fee: Free FDIC-insured: Yes (via Middlesex Federal Savings)

Novo has carved out a distinctive niche by building deep integrations with the tools that small e-commerce businesses actually use. Its native connections with Shopify, Stripe, Etsy, PayPal, and Square mean that your payment platform data flows directly into your banking dashboard. You can see what came in from Shopify last week without logging into three different platforms.

The free account includes unlimited invoicing, expense management, and a reserve feature that lets you set aside money for specific purposes (similar to Relay’s multi-account structure but within a single account). There’s no minimum balance and no monthly fee.

Novo’s Boost feature is worth mentioning: it offers cash back or credits from business tools, including Stripe, HubSpot, and Google Ads, which can add up meaningfully for businesses actively spending on these platforms.

The limitation is that Novo is built for smaller, simpler operations. If you have multiple employees who need their own cards and spending controls, or if you need more than basic cash management, you’ll hit the ceiling of what Novo offers fairly quickly.

For businesses also juggling inventory and sales management, combining Novo with one of the best Shopify apps can create a fairly complete operational stack at very low cost.

Best for: Solo founders, freelancers, and e-commerce sellers on Shopify or Etsy who want free banking with tight platform integration.

5. Lili

Best for: Freelancers, independent contractors, self-employed professionals. Monthly fee: Free; Pro at $17/month; Smart at $35/month. FDIC insured: Yes (via Choice Financial Group)

Lili was designed with one type of business owner in mind: the person who is both the business and the employee. Freelancers, consultants, independent contractors, and self-employed professionals who blend personal and business finances (even when they know they shouldn’t) will find Lili actively helpful in cleaning that up.

The app automatically categorises transactions for tax purposes, tracks deductible expenses in real time, and generates tax reports at year-end that you can hand directly to your accountant. The free plan handles the basics. The Pro plan adds invoicing, unlimited expense categories, and a BalanceShield feature that transfers money from savings to cover potential overdrafts automatically.

What Lili does better than almost anyone else on this list is reduce tax anxiety for self-employed people. The built-in tax bucket feature lets you automatically set aside a percentage of every incoming payment for taxes, which solves the painful surprise of a large tax bill in April.

For freelancers also managing their financial life beyond business banking, our roundup of the best finance apps covers tools that complement what Lili handles on the business side.

Best for: Freelancers and self-employed professionals who want automated tax prep, expense tracking, and simple invoicing without paying for enterprise-level features they don’t need.

6. Found

Best for: Solopreneurs, side business owners, and gig workers. Monthly fee: Free; Plus at $19.99/month. FDIC insured: Yes (via Piermont Bank)

Found sits in a similar space to Lili but with a slightly broader target audience that includes gig workers and people running side businesses alongside full-time employment. The app’s standout feature is its automatic tax withholding: every time money comes in, Found sets aside a calculated percentage for federal and state taxes based on your income and filing status.

The invoicing tool is clean and fast. You can send a professional invoice directly from the app in under two minutes, which is more than most small business owners can say about their current invoicing setup. Payments can be collected via ACH or card, and the paid plan adds the ability to accept credit card payments with a competitive processing rate.

Found’s bookkeeping features are built for simplicity rather than depth. That’s a feature if you’re a solo operator who wants clean records without an accounting learning curve. It becomes a limitation as your business grows and you need more granular reporting.

For businesses growing beyond solo operations who need more robust project and task coordination alongside their finances, our guide to project management tools pairs well with what Found handles on the financial side.

Best for: Side business owners, gig workers, and early-stage solopreneurs who want automated tax handling and simple invoicing without accounting complexity.

7. Brex

Best for: Funded startups, companies with significant monthly spend. Monthly fee: Free for startups; Enterprise pricing for larger companies. FDIC insured: Yes (via partner banks, sweep network up to $6M)

Brex is in a different league from most of the neobanks on this list in terms of what it offers, and also in terms of who it’s designed for. If your startup has raised funding or generates substantial monthly revenue, Brex starts making a lot of sense. If you’re a solo freelancer or early-stage business with minimal spend, it’s overkill.

The Brex card offers one of the strongest rewards programs available to small businesses: points on every transaction, with good rates on software subscriptions, travel, and restaurant spending. The corporate card has no personal guarantee requirement, which matters enormously for founders who don’t want their personal credit tied to business spending.

Brex’s AI-powered spend management features in the 2026 version automatically enforce spending policies, flag out-of-policy transactions, and generate expense reports with minimal human input. For finance teams at growing companies tired of chasing receipts, automation is a real time-saver.

The minimum spend threshold to justify Brex is a consideration. Businesses spending less than $5,000 to $10,000 a month won’t see the full value of the rewards and features. This is a tool for a specific growth stage, not a universal recommendation.

Best for: Venture-backed startups and high-revenue small businesses that want premium corporate spend management, rewards, and no personal guarantee requirements.

8. NorthOne

Best for: Restaurants, retail shops, service businesses with cash operations. Monthly fee: $10/month flat FDIC insured: Yes (via The Bancorp Bank)

NorthOne solves a problem that several other neobanks on this list ignore entirely: physical businesses that deal with cash. Through a partnership with Green Dot, NorthOne customers can deposit cash at over 90,000 retail locations, including CVS, Walmart, and 7-Eleven, across the US. That feature alone separates it from Mercury, Relay, and most competitors.

The $10 flat monthly fee is transparent and predictable, with no per-transaction charges and no minimum balance requirements. The account includes unlimited sub-accounts (called Envelopes) for organizing funds by purpose, solid integrations with QuickBooks and Wave, and a Mastercard business debit card.

NorthOne’s dashboard is built for businesses that need a quick daily financial snapshot: how much came in, what went out, and what’s sitting in each envelope. It’s not the most feature-rich platform on this list, but for a restaurant owner who needs to know if last night’s revenue covers next week’s food order, that clarity is exactly what’s needed.

Managing a physical location also means managing a lot of moving parts beyond banking. Our roundup of the top 10 calendar apps for businesses is worth a look for physical business operators juggling bookings, staff schedules, and deliveries.

Best for: Restaurants, retailers, and service businesses with physical locations that need cash deposit capability alongside digital banking features.

9. Tide

Best for: UK freelancers, sole traders, small businesses. Monthly fee: Free; Plus at £9.99/month; Pro at £18.99/month. FDIC insured: N/A (FCA regulated, FSCS protection applies)

Tide is the dominant neobank for small businesses in the UK and has been for several years. Over 600,000 UK businesses use it, making it the market leader in its category by a significant margin. The free account handles everyday banking, expense categorisation, and invoicing. Paid tiers add cashback on card spending, dedicated customer support, and multi-user account access.

What Tide does particularly well is connect directly to HMRC’s Making Tax Digital framework, which is essential for UK businesses navigating VAT filing requirements. The integration means your transaction data flows into compliant tax records without manual data entry, which saves real time for small business owners who handle their own bookkeeping.

Tide also integrates with Xero, Sage, FreeAgent, and QuickBooks, covering the main accounting platforms used by UK businesses. Customer support is chat-based, which is standard for neobanks, though Tide’s response times are generally faster than most competitors based on Trustpilot data from Q1 2026.

Best for: UK-based sole traders, freelancers, and small businesses that want a leading domestic neobank with strong HMRC and accounting integrations.

10. Revolut Business

Best for: Import/export businesses, international e-commerce, businesses paying global contractors. Monthly fee: Free; Grow at £19/month; Scale at £79/month. FDIC insured: FCA regulated (UK); varies by country

Revolut Business solves a specific and painful problem: dealing with multiple currencies without getting destroyed by conversion fees. If your business pays international suppliers, employs contractors in different countries, or sells in multiple currencies, Revolut’s multi-currency accounts are genuinely transformative compared to what traditional banks charge for the same function.

You can hold over 25 currencies in the same account, convert between them at the interbank rate (or near it on paid plans), and pay international invoices without the 2% to 4% conversion fees that traditional banks apply. For a business moving $20,000 a month internationally, that’s potentially $400 to $800 saved per month on fees alone.

The free plan is reasonably functional, though the currency exchange limits and transaction caps on the free tier make paid plans necessary for businesses with meaningful international volume. The expense management, receipt capture, and team card features are comparable to those of other neobanks on this list.

For businesses also managing international payments at the customer end, rather than just the supplier end, pairing Revolut with one of the best payment gateways for businesses creates a fairly comprehensive international payment setup.

Best for: Businesses with international operations, global contractors, or multi-currency payment needs who want to eliminate unnecessary conversion fees.

How to Choose the Right Neobank for Your Business?

The decision comes down to four questions:

Do you deal with cash? If yes, your shortlist is NorthOne or Bluevine (Green Dot network). Most neobanks skip cash entirely, and that’s a dealbreaker for physical businesses.

Do you need credit alongside banking? Bluevine is the cleanest answer. Brex works if you’re at a growth stage with significant monthly spend. Everyone else on this list is banking only.

Are you a solo operator or do you have a team? Lili and Found are built for solo operators. Mercury, Relay, Brex, and NorthOne are designed to scale with teams and multiple cardholders.

Are you US-based, UK-based, or international? Tide is the UK answer. Revolut Business handles multi-currency international operations better than anyone. The rest are primarily US-focused.

Understanding these fintech tools in a broader context matters too. Our top 10 fintech trends for 2026 show where neobanking sits within the larger shift happening in business finance right now.

What Neobanks Still Can’t Replace?

Neobanks are not full-service banks in the traditional sense. Most don’t hold your deposits directly. They use partner banks for FDIC insurance, which means your funds are protected, but the neobank itself is the intermediary. That’s fine for most small businesses, but worth understanding.

They also generally don’t offer SBA loans, business mortgages, or complex treasury services. For businesses that need those products, a traditional bank relationship is still necessary. The practical approach most small business owners are landing on in 2026 is a neobank as the primary operational account (for its speed, integrations, and lower cost) plus a traditional bank relationship maintained for credit and lending purposes.

Security is a real consideration, too. Neobanks invest heavily in digital security, and most offer features like instant card freezing and real-time transaction alerts. But the broader topic of protecting your business finances digitally goes beyond banking tools alone. Our complete cybersecurity toolkit for SMBs covers the full picture of digital security for small businesses.

Best Neobank FAQs

Yes, provided the neobank uses an FDIC-insured partner bank, which most reputable ones do. Your deposits are typically insured up to $250,000. Always verify the partner bank and FDIC status before opening an account with any neobank.

For many small businesses, yes. Neobanks handle daily transactions, payroll, and vendor payments well. However, if you need an SBA loan, business line of credit, or complex treasury services, you may still need a traditional banking relationship alongside your neobank.

Lili and Found are both purpose-built for freelancers and self-employed professionals. Lili has stronger automated tax tools. Found has cleaner invoicing. If you regularly deal with international clients, Revolut Business is worth considering for its multi-currency handling.

Most do. Relay, Bluevine, NorthOne, Mercury, and Tide all offer direct integrations with QuickBooks, Xero, or both. Always verify the current integration status before choosing, as these partnerships occasionally change with software updates.

Neobanks operate entirely digitally with no physical branches. They typically offer lower fees, faster account opening, and better tech integrations than traditional banks. Traditional banks offer a broader range of financial products, including loans, mortgages, and in-person services.

Novo is purpose-built for e-commerce with native Shopify, Stripe, and Etsy integrations. Mercury is a strong second choice for e-commerce businesses that need more team features and a higher transaction volume. Bluevine works well if you also need access to working capital.

- Kubernetes vs Docker: Which One Do You Need in 2026? - June 24, 2026

- FlexClip AI Long Video to Short Video Review - June 17, 2026

- The Screen Is the New Casino Floor - May 15, 2026