If you’ve been building fintech products for a while, you already know the pain. Getting access to real bank data without drowning in compliance paperwork used to feel almost impossible. Open banking APIs changed that game completely. Now, a developer can pull a user’s transaction history, initiate payments, or verify account balances in a few lines of code, without writing a single letter to a bank’s legal team.

But here’s the thing: not every open banking API platform is built the same. Some are rock-solid for the UK and Europe, others shine in the US, and a few are quietly building global coverage. If you’re a fintech developer trying to pick the right stack, the choice matters more than most people admit.

Let’s cut through the noise. Here are the top 10 open banking API platforms worth your time in 2026, with real insights on what makes each one tick.

What Is an Open Banking API Platform (And Why Should Developers Care)?

Open banking APIs let fintech apps connect directly to banks and financial institutions, with user consent, to read financial data or trigger payments. The concept is simple: instead of users typing their bank credentials into a third-party app (risky, and honestly kind of terrifying), they authorize secure access through a standardized interface.

The UK’s Open Banking Standard, the EU’s PSD2 directive, and similar frameworks in India, Australia, and the US have turned this from a niche experiment into a mandatory infrastructure layer for any serious fintech product. According to the Open Banking Implementation Entity (OBIE), there are now over 11 million active open banking users in the UK alone, and that number keeps climbing.

For developers, this means two things. First, the demand for apps built on top of these platforms is massive. Second, the platforms themselves have matured enough that you can actually build production-ready products on them without losing your mind. If you want a broader view of how these tools fit into the fintech ecosystem, check out this guide to fintech tools for businesses before diving in.

Top 10 Open Banking API Platforms for Fintech Developers

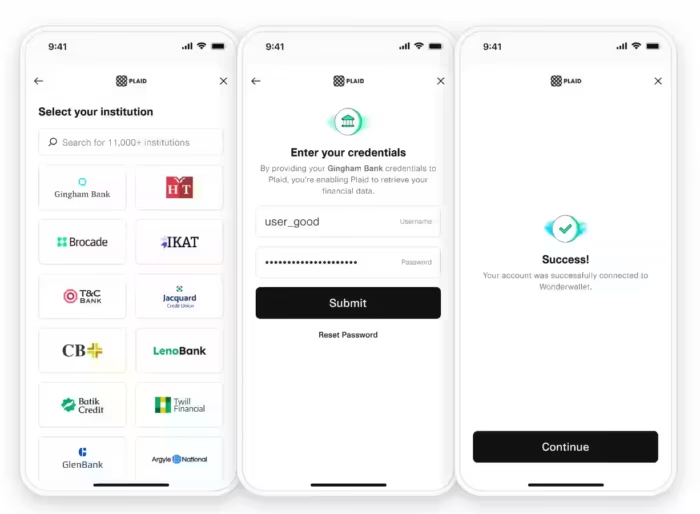

1. Plaid

Let’s start with the name everyone in North American fintech knows. Plaid is, for most US-based developers, the default starting point. It connects to over 12,000 financial institutions across the US, Canada, and parts of Europe, and its API documentation is genuinely one of the best in the industry.

What makes Plaid stand out is how much ground it covers. You can pull transaction data, verify account and income information, authenticate bank accounts for ACH transfers, and even check investment holdings, all through a unified interface. The Plaid Link UI component drops right into your app with minimal setup, which is a serious time-saver.

The catch? Cost. Plaid’s pricing has been a point of frustration for early-stage startups. It’s not the cheapest option once you scale, and there have been occasional reliability complaints from developers during high-traffic periods. Still, for US-focused products, it’s hard to argue against Plaid’s depth of institutional coverage.

Best for: US and Canadian fintech apps, personal finance tools, and lending platforms.

2. Truelayer

If Plaid is the American standard, Truelayer is the European equivalent. Built from the ground up for PSD2 compliance, Truelayer covers the UK, Ireland, France, Germany, Spain, Italy, and several other European markets. Their coverage is genuinely impressive, with connections to hundreds of banks across the continent.

What I personally appreciate about Truelayer is how clean their developer experience feels. Their sandbox environment is responsive, their webhook system is reliable, and their data enrichment layer (which categorizes and normalizes transactions) is better than most competitors. For anyone building in the UK open banking space, Truelayer is often the first recommendation.

They also offer payment initiation, meaning you can trigger bank transfers directly through the API, not just read data. That opens up some genuinely interesting use cases, like instant refunds, split payments, and subscription billing without card rails.

Best for: UK, EU, and Irish market products, payment initiation, and financial data aggregation.

3. MX Technologies

MX takes a different angle than most platforms on this list. Rather than just connecting to bank accounts, MX focuses heavily on financial data intelligence. They clean, categorize, and enrich transaction data at scale, making sense of the messy raw data that banks actually send.

Their platform connects to over 16,000 financial institutions worldwide, which is a bigger number than most people realize. What makes MX interesting for developers is their focus on financial wellness use cases. Their APIs aren’t just designed for reading balances; they’re built to help apps deliver insights, spending analysis, net worth tracking, and budgeting features.

If you’re building a personal finance app or a financial health product for a bank’s customer base (MX powers many white-label bank apps), MX is a serious contender. The API is clean, the support team is responsive, and their data models are well-thought-out. That said, their pricing structure is enterprise-focused, so solo developers or very early startups might find it harder to access.

Best for: Personal finance apps, bank white-label products, and financial wellness platforms.

4. Yapily

Yapily is a UK-based open banking platform with genuinely global ambitions. They cover over 2,000 financial institutions across 18 countries, with particularly strong coverage in Europe and a growing presence in Latin America. Their API is notably clean and consistent, which matters more than you might think when you’re dealing with the messiness of bank integrations.

One thing developers tend to appreciate about Yapily is their raw API-first approach. There’s no pre-built UI forcing you into a specific user flow. You get the data and connections, and you decide how to surface them. That flexibility is genuinely valuable if you’re building something custom.

They’re also transparent about their data, which is refreshing in a space where some platforms are oddly cagey about what they actually connect to. Their documentation specifies exactly which banks support which data types, so you’re not flying blind when scoping a project.

Best for: European fintech, custom UI/UX builds, multi-country payment apps.

5. Finicity (by Mastercard)

Acquired by Mastercard in 2020, Finicity brings serious credibility and infrastructure to open banking. Their platform specializes in financial data verification, particularly for lending and mortgage use cases. If you’re building a lending product that needs to verify income, assets, or employment, Finicity is one of the strongest options available.

Their partnership with Mastercard gives them connections that smaller providers can’t match. They work directly with major US financial institutions, and their data is trusted by lenders, credit bureaus, and mortgage servicers. Fannie Mae and Freddie Mac have both validated Finicity’s data for mortgage applications, which is a meaningful endorsement.

The developer experience is solid but not flashy. It gets the job done. For consumer lending, mortgage tech, and credit underwriting applications, Finicity’s specialized data is genuinely hard to beat.

Best for: Lending platforms, mortgage tech, income, and asset verification.

6. Salt Edge

Salt Edge deserves more attention than it gets in mainstream fintech conversations. Based in Canada with operations across Europe and the Middle East, Salt Edge connects to over 5,000 financial institutions in more than 60 countries. That global footprint is a real differentiator.

Their compliance framework is notably thorough. Salt Edge is PSD2 compliant, FCA registered, and holds several other regional certifications. For fintech startups worried about regulatory exposure, that compliance track record matters. They also offer a dedicated sandbox with realistic test data, which makes development and QA significantly smoother.

Salt Edge’s pricing is more accessible than some enterprise-only competitors, making it a viable choice for earlier-stage startups building internationally. Their developer documentation is solid, though not quite as polished as Plaid or Truelayer. Worth exploring if you need multi-region coverage without enterprise-level pricing. This is especially relevant if you’re looking at top fintech trends in 2026 and trying to build for global markets from day one.

Best for: International fintech, Middle Eastern and African markets, compliance-first builds.

7. Tink (by Visa)

Tink was one of Europe’s most respected open banking infrastructure companies before Visa acquired it in 2022. That acquisition gave Tink significant resources, and the platform has continued to improve. They cover 18 European markets with connections to over 3,400 financial institutions.

What makes Tink interesting post-acquisition is the combination of its open banking infrastructure with Visa’s payment network. The integration possibilities are genuinely compelling. Developers can build account-to-account payment flows, financial data products, and risk assessment tools, all through a platform that now has Visa’s institutional relationships behind it.

Their developer portal is well-organized, and their sandbox environment is reliable. The main limitation is geographic. If you’re building outside of Europe, Tink isn’t the answer. But for European products, they’re one of the most mature and well-resourced options available.

Best for: European market products, account-to-account payments, and Visa ecosystem integrations.

8. Nordigen (by GoCardless)

Nordigen built its reputation on something that sounds almost too good: free access to bank account data across Europe, funded through the open banking regulations that require banks to provide API access at no charge. GoCardless acquired them in 2023 and has been building them into a broader payments infrastructure.

For developers building in Europe who need account information (balances, transactions, account details), Nordigen’s pricing model is genuinely compelling. Payment initiation features have pricing, but the data access tier is hard to compete with in terms of cost. This makes Nordigen particularly attractive for startups validating a product concept without a big infrastructure budget.

The platform covers 2,300 banks across 31 European countries. Their API is straightforward, their onboarding is faster than most competitors, and their GoCardless integration opens up useful direct debit capabilities for subscription products. If you’re considering payment gateway options as part of your stack, it’s worth seeing where Nordigen fits alongside traditional payment processors.

Best for: European startups, data-heavy applications, budget-conscious development teams.

9. Basiq

Australia’s open banking story has been slower to develop than Europe’s, but it’s picking up momentum fast. Basiq is the platform that most Australian fintech developers reach for first. They connect to over 100 Australian financial institutions and have built their platform specifically around Australia’s Consumer Data Right (CDR) framework.

Their API is clean and well-documented, with particularly strong support for Australian bank account types and transaction structures. For anyone building budgeting tools, lending products, or financial health apps for the Australian market, Basiq is the obvious starting point.

What I find genuinely impressive about Basiq is how thoughtfully they’ve handled consent management. The CDR framework has specific requirements around how users grant and revoke consent, and Basiq’s implementation handles that complexity gracefully. It’s one of those things that sounds boring until you’re three weeks into a build and realize how much it matters.

Best for: Australian fintech apps, CDR-compliant products, budgeting and personal finance tools.

10. Stripe Financial Connections

If you’re already building on Stripe, Financial Connections is the path of least resistance for adding bank account verification and basic financial data to your product. It connects to thousands of US financial institutions and handles the OAuth flow, data normalization, and user interface in a way that’s very on-brand for Stripe: opinionated but effective.

The main appeal is integration simplicity. If your payment infrastructure already lives in Stripe, adding Financial Connections doesn’t require a new vendor relationship, new contracts, or major architecture changes. You get bank account verification, real-time balance checks, and transaction history, all in the Stripe ecosystem.

The limitation is obvious: Financial Connections is US-focused and doesn’t try to be a comprehensive open banking platform. It’s a feature within a payments platform, not a standalone open banking solution. But for the use cases it covers, it’s remarkably smooth to implement. Pair it with other money transfer apps or payment tools, depending on your product’s specific needs.

Best for: Stripe-native products, US bank verification, payment-adjacent data use cases.

How to Choose the Right Open Banking API Platform

There’s no single right answer here. The decision usually comes down to four factors: geography, use case, pricing model, and how much flexibility you need in the user interface.

Geography is the most obvious filter. Plaid for North America, Truelayer or Tink for Europe, Basiq for Australia, Salt Edge if you need genuinely multi-regional coverage. Start there.

Use case matters more than most developers initially think. MX and Finicity are built for lending and financial wellness. Nordigen and Yapily lean toward clean data access. Stripe Financial Connections is optimized for payment verification. Match the platform to the problem, not the other way around.

Pricing is where things get tricky. Several platforms don’t publish pricing openly, which is frustrating. Build in time to actually talk to sales teams if you’re evaluating enterprise-tier platforms like MX or Finicity. For earlier-stage projects, Nordigen’s pricing model and Salt Edge’s startup-friendly tiers are worth exploring first.

Finally, think about how much control you want over the user experience. Plaid Link and Stripe Financial Connections are opinionated UI components that do the heavy lifting but don’t leave you much room to customize. Yapily and Truelayer give you more raw API access to build your own flows. Neither approach is wrong, but the choice affects your development timeline significantly.

For a broader look at what’s driving fintech development decisions in 2026, including regulatory shifts and infrastructure trends, this overview of top fintech trends is worth a read.

What About Security and Compliance?

This question comes up in every developer conversation about open banking, and rightly so. The short answer: reputable platforms on this list handle the heavy compliance lifting, but you still carry responsibility for how you store, use, and protect user data.

Every platform here uses OAuth 2.0 for authorization, meaning users grant explicit consent and can revoke access at any time. None of these platforms store user bank credentials. The data flows through encrypted channels, and the major platforms maintain SOC 2 Type II certifications, FCA registration, and other relevant regulatory approvals.

What you’re responsible for is your own application layer: data retention policies, user consent records, security testing, and data minimization practices. Don’t collect data you don’t need. If you’re building something that touches financial data at scale, a proper security review is non-negotiable.

A Quick Note on Emerging Markets

One thing this list doesn’t fully address is Southeast Asia, India, and Africa, markets where open banking is developing fast but through different frameworks. India’s Account Aggregator framework is particularly interesting, built on top of the existing UPI infrastructure that already processes billions of transactions per month. Developers building for Indian users should explore AA-compliant platforms rather than forcing a Plaid or Truelayer integration that won’t match local bank coverage. The e-wallet landscape in India gives a useful context for how payment infrastructure has evolved there.

Africa and Southeast Asia are moving toward open finance rather than just open banking, which is a broader framework that includes insurance, investments, and pension data. Keep an eye on Stitch (South Africa) and Brankas (Southeast Asia) if those markets are in your roadmap.

Conclusion

Open banking API platforms have made building serious fintech products dramatically more accessible than they were five years ago. The infrastructure is there. The regulatory frameworks are maturing. The developer experience has improved across the board.

The real question now isn’t whether to use an open banking platform; it’s which one fits your specific product, market, and team. Go back to the beginning of this post: what geography are you targeting? What problem are you actually solving? That’s where your decision starts.

For most US developers, Plaid is still the default worth serious evaluation. For Europe, Truelayer and Tink are both genuinely excellent. If you’re bootstrapped or cost-conscious, Nordigen’s pricing model is compelling. And if you’re building globally, Salt Edge’s multi-region coverage deserves more credit than it usually gets.

- Kubernetes vs Docker: Which One Do You Need in 2026? - June 24, 2026

- FlexClip AI Long Video to Short Video Review - June 17, 2026

- The Screen Is the New Casino Floor - May 15, 2026