Last Updated: April 2026 | Pricing and features change. Verify directly with vendors before committing.

Fintech tools for businesses are software platforms and digital services that automate financial operations, from payments and accounting to lending and compliance. Over 56% of SMEs already use them (DemandSage), and the reason isn’t loyalty to innovation. It’s that traditional banking no longer makes practical sense for many day-to-day business finance needs.

If you’re still bouncing between a bank portal, a spreadsheet, and your accountant’s inbox to figure out where your cash actually is, this guide is for you. We’ll cover what these tools actually do, which ones are worth your time, and how to think through building a stack that fits your business rather than somebody else’s.

What Fintech Tools Actually Do (And Why Banks Struggle to Compete)

You need to pay a contractor in Portugal today. Your bank wants three to five business days, a SWIFT code, a branch visit maybe, and a fee you won’t see until it’s already gone. A fintech payment tool does it in minutes, shows you the exact exchange rate upfront, and automatically emails you a receipt.

That’s a small example, but it captures the core difference. Traditional banks were built around physical infrastructure, compliance bureaucracy, and a customer base that didn’t have alternatives. Fintech platforms were built around the opposite: API-first, fast, transparent, and designed to integrate with everything else in your workflow.

The Financial Technology Association found that 98% of small businesses say fintech serves them better than traditional banks. I’d argue that number would’ve been unthinkable a decade ago. And Plaid’s 2026 Fintech Trends Report puts fintech app usage at 78% among consumers, up 20 points since 2020. The adoption curve isn’t slowing.

Globally, the fintech market sits at $460.76 billion in 2026 (Fortune Business Insights), projected to reach $1.76 trillion by 2034. That’s an 18.2% annual growth rate, which is the kind of trajectory that reflects real utility, not hype. People don’t keep paying for things that don’t work.

What’s changed most recently is the AI layer. Fraud detection that adapts in real time, reconciliation that runs without anyone touching it, and cash flow forecasting that actually accounts for your seasonal patterns. The AI in the fintech market is already worth $17.69 billion (The Business Research Company) and is on track to nearly triple by 2029. We’re well past the buzzword phase on this one.

The 6 Types of Fintech Tools (And What Each One Is Actually Solving)

Most businesses don’t need one fintech tool. They need a few, each doing a specific job. The confusion usually comes from vendors marketing themselves as everything, when really they’re strong in one or two areas and thin everywhere else.

Payments and Transaction Processing

The starting point for most businesses. Card payments, invoicing, international transfers, subscription billing, anything involving money moving between parties. These platforms tend to integrate with everything downstream, so getting this layer right matters more than most founders initially realize.

Key tools: Stripe, Square, Wise Business

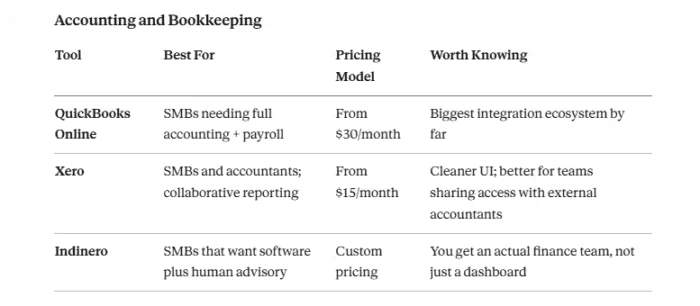

Accounting and Bookkeeping Software

Once money is moving, someone needs to track it. Modern accounting fintech replaces manual data entry with automated categorization, live bank syncing, and reporting you can actually read without an accounting degree.

Key tools: QuickBooks Online, Xero, Indinero

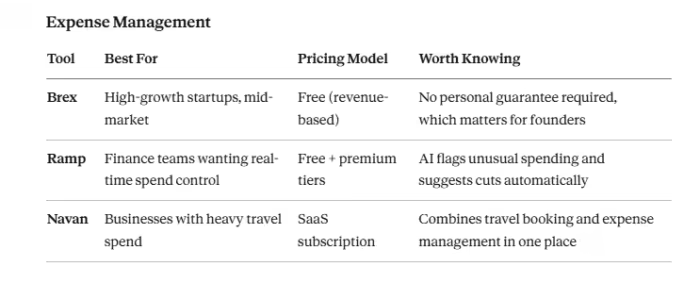

Expense Management and Spend Control

The moment you hire your fifth employee, expense reports become a minor organizational disaster. Corporate cards paired with spend management software give finance teams real-time visibility into what’s being spent, by whom, on what, before the month-end surprise.

Key tools: Brex, Ramp, Navan

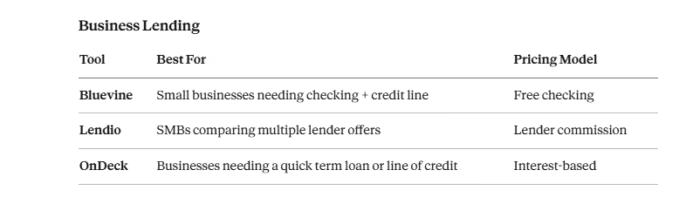

Business Lending and Financing

Fintech lenders use algorithm-driven underwriting instead of the traditional bank process, which can drag on for weeks. Decisions come in 24 to 48 hours. Some platforms aggregate multiple lenders so you can compare actual offers without submitting five separate applications.

Key tools: Bluevine, Lendio, OnDeck

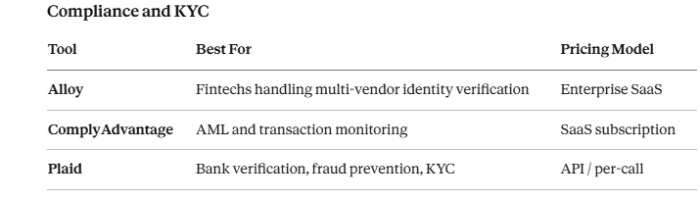

Compliance, KYC, and AML Tools

This is the category most guides gloss over, which is strange because in 2026 it’s arguably the most consequential one. MiCA, AML, KYC, PCI-DSS. Regulatory requirements for businesses handling payments at any real scale are not optional, and the cost of getting them wrong is high. RegTech tools automate identity verification, transaction monitoring, and audit trails.

Key tools: Alloy, ComplyAdvantage, Plaid

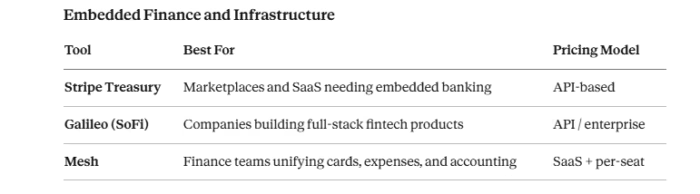

Embedded Finance and Banking Infrastructure

More relevant if you’re building a platform or marketplace than if you’re running a traditional SMB. Embedded finance lets non-financial companies offer financial products inside their own product, think a SaaS platform giving users a business bank account, or a marketplace enabling instant seller payouts. Companies like Stripe, Treasury, and Galileo have made this genuinely accessible to businesses that aren’t traditional financial institutions.

Key tools: Stripe Treasury, Galileo (SoFi), Plaid

The Tools Themselves: A Category-by-Category Breakdown

Tables help here, so let’s use them. But the numbers only tell part of the story, so I’ll add context after each one.

Payment and Global Transfers

Stripe is the obvious recommendation for anything subscription-based or platform-driven, though it does assume you have someone technical to set it up properly. Square is the better fit for businesses with a physical presence who want one system across in-store and online. And Wise Business is worth knowing about if you’re paying international contractors regularly. Bank wire fees on international transfers are quietly one of the higher unnecessary costs for small businesses, and Wise eliminates most of that overhead.

Accounting and Bookkeeping

QuickBooks wins on integrations. If your accountant already lives in it, switching has a real switching cost. Xero is genuinely better software in a lot of ways, particularly for companies with accountants working remotely or across time zones. Indinero is a different animal entirely. It’s not just software. You get a finance team embedded in the platform, which makes sense the moment your business has outgrown a spreadsheet, but you’re not ready to hire a full-time CFO.

Expense Management

Ramp has become genuinely useful beyond just being a corporate card. The AI layer spots patterns in spending that most finance teams wouldn’t catch manually until month-end. Brex makes more structural sense for startups because the credit limits scale with revenue rather than personal credit history, which removes a barrier that trips a lot of founders up early on.

Business Lending

If you’re not sure what financing structure makes sense, Lendio is a reasonable starting point. One application surfaces offers from multiple lenders, which, at minimum, gives you a clear picture of what you actually qualify for. OnDeck suits businesses that already know they need capital quickly and prefer dealing with one lender directly rather than comparing.

Compliance and KYC

Plaid’s 2026 report flagged US fraud losses at $12.3 billion in 2023, with AI-driven fraud projected to reach $40 billion by 2027. That’s not a background stat. Businesses that treat compliance tooling as something to figure out later tend to find out the cost of that decision at the worst possible moment.

Before You Pick Anything, Answer These Five Questions

Buying tools based on what’s getting buzz is how businesses end up with four overlapping subscriptions and a messy integration problem. Start with your actual constraints.

What’s the specific pain you’re trying to solve?

Not “financial efficiency.” The actual problem. International payments taking too long? No visibility into what your team is spending? A lender asking for audited financials you don’t have? The answer to that question determines which category you need first, and probably which ones you don’t need yet.

What compliance obligations are actually on you?

Processing card payments means PCI-DSS applies. Running KYC on users means you need a verified identity provider. Sending money internationally at volume means AML requirements enter the picture. Before signing any vendor contract, ask specifically whether they hold SOC 2 Type II certification. No cert is a meaningful red flag. And if you’re expanding into European markets, MiCA compliance is now a live concern, not a future planning item.

What does your current stack look like?

A tool that doesn’t talk to your accounting software creates more manual work than it eliminates. Most major platforms have native integrations with QuickBooks, Xero, and Salesforce. But “integration” can mean anything from a real-time sync to a monthly CSV export you have to manually upload. Ask exactly how it works before committing.

What does this actually cost at your real volume?

Pricing pages are built to show the most attractive number. Transaction fees, per-seat charges, API call limits, and premium support tiers. Get a 12-month cost projection based on your actual transaction volume and team size, not the base plan example. Then model it at 3x your current volume, because that’s usually when the pricing structure starts to matter.

Can you test it before going live?

Every serious platform offers a sandbox environment for testing. If a vendor resists that request, that tells you something useful. The good products make the trial period easy because they’re not worried about what you’ll find.

A rough stack by stage, for reference:

- Pre-revenue to $1M ARR: Stripe + Brex + Xero covers most of what you need without overcomplicating things

- $1M to $10M ARR: Add Ramp for spend control, Lendio when you need financing options, Plaid for bank data connectivity

- $10M+ ARR: Look seriously at Alloy or ComplyAdvantage for compliance, and evaluate Stripe Treasury or Galileo if you’re building embedded finance into your product

What’s Shifting in Fintech Right Now

A few things are changing how these tools work and what they can do. Worth knowing before you make long-term platform decisions.

AI Has Moved Past the Marketing Phase

In 2023, every fintech tool added “AI-powered” to its homepage. In 2026, the ones that actually built it out are separating from the ones that didn’t. Real-time fraud detection that learns from new attack patterns. Automated reconciliation that catches errors before any human notices. Cash flow forecasting with enough context to reflect your specific business cycles.

Plaid found that 57% of consumers now specifically want AI features in their fintech apps. On the business side, that demand runs higher. Tools like Ramp are already surfacing cost-reduction suggestions automatically, not as a feature you have to turn on. That’s where the whole category is heading.

Real-Time Payments Are Quietly Becoming the Default

The RTP network saw transaction volume jump 28% in Q4 2025, with transaction value up 405% (The Clearing House). That second number is the more interesting one. It’s not just more payments. It’s significantly larger payments moving through real-time rails. Businesses still relying on two-to-three-day ACH for supplier payments and contractor payouts are introducing friction that competitors settling instantly don’t have.

The Stablecoin and Open Banking Picture

$23 trillion in stablecoins were traded in 2024, up 90% year over year (Plaid 2026 Trends Report). That figure surprises most people. For B2B cross-border payments, especially in markets with volatile local currencies, stablecoins are increasingly a practical option rather than a speculative one. Whether it applies to your business depends heavily on your geography and supplier base.

Open banking is the quieter version of the same underlying shift. APIs that let your lender assess creditworthiness based on actual cash flow instead of a credit score. Your accounting software is pulling live transaction data without anyone manually importing a file. KPMG’s Pulse of Fintech H2 2025 flagged this as actively reshaping how business credit decisions get made, and Plaid is the primary infrastructure layer for most of this in the US.

The Honest Downsides (That Most Guides Skip)

Getting out is harder than getting in

Some platforms make data portability deliberately difficult. Before you go deep with any tool, ask: can you export your complete transaction history in a portable format? What does the offboarding process look like? These questions feel academic until the day you actually need the answers, at which point they suddenly feel very urgent.

The fee math changes at scale

The base plan always looks reasonable. It’s when your volume hits the next tier, or you realize a feature you depend on is locked behind a premium plan, that the real cost structure becomes clear. Model pricing at 3x your current usage before signing. The platforms worth using can usually justify the cost at scale. The ones that can’t tend to hope you won’t notice until you’re already committed.

Your compliance obligation doesn’t transfer to the vendor

Alloy handling your KYC doesn’t mean your compliance exposure is fully covered. Depending on your industry and the geographies you operate in, independent audits may still apply. KPMG’s Pulse of Fintech H2 2025 flagged regulatory complexity as one of the top concerns for businesses scaling fintech globally. If you’re expanding internationally, get proper legal advice. Assuming the tool covers it is a mistake businesses make more often than you’d think.

Support quality is not evenly distributed

Fintech tools are SaaS products, and SaaS support ranges from genuinely excellent to basically nonexistent. For anything touching your payment processing or banking layer, ask about the support SLA explicitly before you sign. A platform that takes 72 hours to respond when your payment integration breaks is not a neutral choice.

Where to Start?

Sit down with whoever handles your finances, whether that’s a CFO, a bookkeeper, or yourself, and answer three questions honestly.

Where is money leaving your business inefficiently right now? Wire transfer fees, manual reconciliation time, late payment penalties, and currency conversion costs on international payments. These tend to be the easiest wins because the cost is already visible, just accepted.

What financial visibility do you currently not have? Real-time cash flow, spend by department, and upcoming payment obligations. If you’re making decisions based on last month’s data, closing that gap is usually the highest-leverage change you can make.

What compliance or security exposure are you carrying? If your KYC process is still manual or you haven’t done a PCI-DSS review, that’s not a “later” category regardless of how busy things are.

Pick one tool in the most urgent category. Pilot it properly. Most of the fintech decisions that go wrong come from buying a full suite upfront before understanding whether the core product fits how the business actually works.

The fintech market is growing at 18.2% annually through 2034 (Fortune Business Insights), which means more competition, better tools, and falling prices in most categories over time. The infrastructure is more accessible than it’s ever been. The question worth sitting with is whether you’re using it in proportion to what it can actually do for you.

Start with the friction. Build from there.

- Cloud Cost Management in 2026: FinOps Strategies That Work - April 5, 2026

- Top 10 Fintech Trends Dominating April 2026 - April 4, 2026

- Ultimate Guide to Fintech Tools for Businesses 2026 - April 3, 2026